November

2020

Webster Hughes, PhD, Managing Principal, Multifamily Comps

This paper presents the

authors’ present opinions reflecting current market conditions, which are

subject to change without notice. It has been written for informational and

educational purposes only and should not be considered as investment advice or

as a recommendation of any particular security, strategy, or investment

product.

Purpose

of This Article

Multifamily

Comps LLC (“MFC”) has

implemented a location-based Demographic Score within its Multifamily

Predictive Analytics System (“MPAS”). The Demographic Score is used to model

the impact of location-based demographic factors on property-level valuation

and operating performance forecasts. This article explains the Demographic

Score calculation, provides an example from the MFC property database, and introduces

a color-coded heat map showing property locations with more or less demographic

risks. The article concludes with an explanation for how MFC Demographic Score

methodology and software can be customized to Client’s specifications and use

cases.

I.

Current Investment Environment

The longest business cycle in the U.S. history ended

abruptly in March 2020 as the public health crisis caused by the COVID-19 virus

spread around the world. The nation’s

economy is now amid one of the most severe recessions in almost a century and

there is high uncertainty with regards to how deep and prolonged this downturn

will be. Now eight months into the

crisis with eviction moratoriums, loan forbearance, and stop-and-start

reopening, real estate investors are grappling with how variations in renter

demographic profiles will likely impact property-level operating performance.

II.

Baseline Economic and Demographic Scenario

Assumptions

MPAS

utilizes Baseline Economic and Demographic Scenario

Assumptions as a starting point to forecast property-level revenue, expenses, CAPEX,

and valuation over forward time periods. Our Baseline Forward Scenario for Revenue

assumes a deep multi-year recession with an uncertain economic re-opening and

substantial variation across demographic profiles due to uneven expected job

loss, renter financial condition, and exposure to the COVID-19 virus. To model the

uneven economic stress across demographic profiles, we implemented a location-based

Demographic Score using Census Data sourced from a 1-mile radius of each

Property in the MFC Database. Our Demographic Score ranges from -10 (lowest economic

stress) to +10 (highest economic stress) based on a risk-weighted average of

Census items which we estimate will impact renter ability-to-pay and property-level

revenue over forward time periods.

Table 1

provides our Baseline Revenue Assumptions for Demographic Scores ranging from

-10 to +10. As the reader can see in the Table 1, we assume wide variation in

Revenue Growth based our Demographic Score. While acknowledging that we have no

historical experience with the impact of a pandemic on property-level, we bring

decades of experience in economic analysis as relates to multifamily,

applications of Census data, and all manner of investment stress analyses. It

is our professional opinion is that this wide variation is warranted and should

be included in any credible effort to forecast operating performance in the

current economic environment.

TABLE 1: Baseline Forward Scenario Assumptions (Revenue)

Industry

researchers often use metro, submarket, zip code level Census averages when

analyzing the effect of demographic factors on property operating performance. Whereas

aggregating over these larger areas may be useful when speaking in

generalities, it is not reliable for property-level analytics. MPAS uses Census

data sourced in a 1-mile radius from each of the 26,000+ properties in our

database. The importance of using tightly localized Census data is noteworthy.

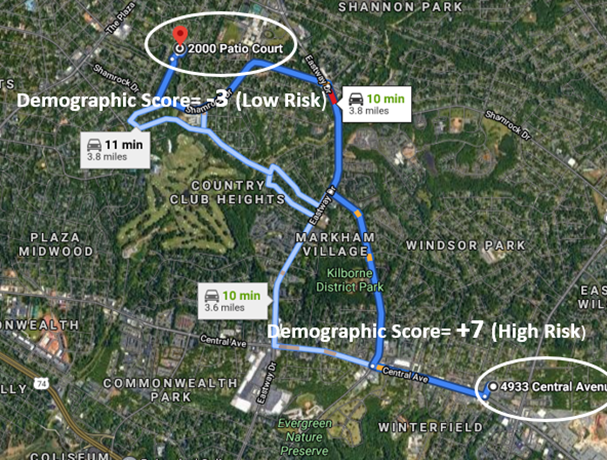

In Table 2 below, we provide an example of two properties located 3 miles apart

in the same Charlotte, NC zip code with opposite Demographic Score.

TABLE 2: Opposite

Demographic Scores in the same Charlotte, NC 28205 zip code

The difference in demographic profile is obvious for anyone who visits the properties. 2000 Patio Court (Demographic Score= -3) is in a leafy neighborhood next to Charlotte Country Club with high concentration of people with college degrees and working in the financial industry; 4933 Central Avenue (Demographic Score= +7) is a densely populated lower income area with high concentration of employment in construction and service industries. Table 1 shows a 12% difference in cumulative Revenue Growth for the two locations. The difference in revenue growth based on demographic profiles feeds directly into MPAS and is a primary determinant of Valuation and Operating Performance Forecasts.

Table 3 below

shows underlying calculations for 4933 Central Avenue (Demographic Score= +7).

It lists the Risk Factors and Risk Mitigants in order of component risk score.

TABLE 3: Demographic Score=+7 (High Risk), Top Risk Factors and Mitigants

III. Color-Coded Heat Map

The www.multifamilycomps.com dashboard includes color-coded heat map

based on Demographic Score (red=high-risk, green=low-risk). The map can be filtered

by Metro, Subtype, Units, and Demographic Score. Table 4 below provides an

example screenshot.

Table 4:

Color-Coded Heat Map for greater TX-Dallas-Fort Worth-Arlington CMSA

The MFC

Demographic Score methodology and software can be readily customized in two different

ways:

1)

Input

a Client’s customized specification of the strength coefficients of the various

Census data risk factors and risk mitigants used to calculate the Demographic

Score.

2)

Apply

either MFC or a Client’s customized specification to a set of locations

provided by the Client. An example

Item #1 above

translates into different Demographic Scores and therefore different MPAS

Valuation and Operating Forecasts. MPAS software applications include templates

for input and testing of a Client’s specifications of different strength

coefficients.

Item #2 above

enables a Client to specify a Demographic Score for any number of purposes and

for any set of locations. An example would an investor or lender using a

customized score to determine geographic acquisition and origination focus.

MFC has technology in place to collect over 300 Census data items sourced from 1, 3, and 5-mile radiuses of any set of locations (specified by either address or geographic coordinates). The Census Data is available historically as well. MFC used the historical data for statistical modeling and forecasts. We welcome customization and software projects using this technology.